CDP Technical Note: Accounting of Scope 2 emissions

CDP Corporate Questionnaire

Page 2 of 27 @cdp | www.cdp.net

Contents

1 ESSENTIAL READING ............................................................................................................. 5

2 INTRODUCTION TO SCOPE 2 ................................................................................................ 6

2.1 KEY CONCEPTS IN SCOPE 2 THAT IMPACT YOUR REPORTING TO CDP .......................................... 6

3 REPORTING YOUR SCOPE 2 EMISSIONS TO CDP .............................................................. 8

3.1 SCOPE 2 EMISSIONS TARGETS, TOTALS, BREAKDOWNS, AND INTENSITY METRICS ........................ 8

3.2 YOUR ACTIVITY DATA AND YOUR CONTRACTUAL INSTRUMENTS .................................................. 9

4 WHAT SCOPE 2 REQUIREMENTS IMPACT YOUR RESPONSE? ....................................... 10

4.1 DETERMINING WHETHER YOU SHALL DUAL REPORT .................................................................. 10

4.2 CHOOSING THE RIGHT EMISSIONS FACTORS (SCOPE 2 DATA HIERARCHY) .................................. 11

4.3 SCOPE 2 QUALITY CRITERIA ................................................................................................... 13

4.4 IF YOU CONSUME ENERGY FROM FACILITIES THAT YOU OWN/OPERATE ...................................... 15

4.5 IF YOU CONSUME PURCHASED ENERGY GENERATED FROM BIOFUELS ........................................ 15

5 OPTIONAL SCOPE 2 DISCLOSURES ................................................................................... 16

6 COUNTRY/AREA RESOURCES FOR EMISSIONS FACTORS ............................................. 17

6.1 LOCATION-BASED EMISSIONS FACTORS .................................................................................. 17

6.2 ENERGY ATTRIBUTE CERTIFICATE REGISTRIES ......................................................................... 17

6.3 SUPPLIER-SPECIFIC EMISSIONS FACTORS ................................................................................ 18

6.4 RESIDUAL MIXES .................................................................................................................... 18

7 FREQUENTLY ASKED QUESTIONS ..................................................................................... 20

8 WORKED EXAMPLES ........................................................................................................... 22

8.1 EXAMPLE 1 – ON-SITE PRODUCTION OF NON-GRID CONNECTED RENEWABLE ELECTRICITY OWNED

BY ANOTHER ORGANIZATION WITH NO TRACKING INSTRUMENTS GENERATED. .................................... 22

8.2 EXAMPLE 2 – A ORGANIZATION PURCHASING RECS IN THE USA.............................................. 25

Page 3 of 27 @cdp | www.cdp.net

Version control

Version

Revision date

Revision summary

1.0

February 8, 2013

First published version.

2.0

February 8, 2015

Updated to take in account new GHG Protocol Scope 2 Guidance and

other necessary updates.

3.0

February 18, 2016

Updated to align with the 2016 CDP climate change questionnaire

4.0

March 21, 2017

Minor updates to align with the 2017 CDP climate change

questionnaire.

5.0

June 7, 2018

Minor updates to align with the 2018 CDP climate change

questionnaire.

6.0

March 12, 2019

Minor updates including:

New countries adherent to the International REC Standard (I-REC

Standard) and Tradable Instruments for Global Renewables (TIGR

Registry) (Section 3)

New clarification on market-based approach (Section 1)

7.0

April 03, 2020

Updated to align with the 2020 CDP climate change questionnaire

including:

Revised structure of the document

Updated Glossary: “low-carbon energy”, “RE100” added

New definition of the market boundary criteria for claiming renewable

electricity use (section 2.3)

New countries adherent to the International REC Standard (I-REC

Standard)

New information about Taiwan and Japan certificate systems

7.1

July 03, 2020

Section 2.3 is updated with information on exemption for renewable

energy sourcing contracts signed before 31st December 2021

8.0

April 12, 2021

Updated to align with the 2021 CDP climate change questionnaire

including:

Revised definitions of green electricity/power, TIGRs and International

REC

Guidance added on questions companies can provide additional

information for

European residual mix figure source updated to AIB

Revised guidance on the use of REGOs in the UK following Brexit

Revised guidance to clarify the use of green gas certificates

9.0

March 11, 2022

Updated to align with the 2022 CDP climate change questionnaire

including:

Clarified guidance on the market boundary criteria exemption

Clarified guidance on best practice of EAC vintage

New information on Chinese GECs

Updated country and regional guidance and resources

10.0

March 7, 2023

Updated to align with the 2023 CDP climate change questionnaire

including:

Clarification of the market boundary criteria in section 2.3.

Clarification on the use of green gas certificates for renewable

electricity usage claims in section 3.5.

11.0

June 28, 2024

Structural changes, clarifications, new introduction.

Page 4 of 27 @cdp | www.cdp.net

About this document

This technical note outlines how your how reporting to CDP should meet the requirements in the

GHG Protocol Scope 2 Guidance. You should have a basic understanding of the Scope 2

Guidance before reading this technical note, especially around the dual reporting requirement, the

scope 2 data hierarchy, and the Scope 2 Quality Criteria.

CDP has an accredited solutions provider program that can connect you with experience and

expertise in scope 2 accounting, scope 2 emissions reductions initiatives (such as renewable

energy procurement), and in reporting these emissions to CDP. For more information about the

program please contact [email protected].

Copyright © CDP Worldwide 2024

All rights reserved. Copyright in this document is owned by CDP Worldwide, a registered charity number

1122330 and a company limited by guarantee, registered in England number 05013650.

Page 5 of 27 @cdp | www.cdp.net

1 Essential reading

Key concept used

in this document

Summary

Please read

Scope 1

Direct GHG emissions occurring from

sources that are owned or controlled by

the reporting organization.

The Greenhouse Gas Protocol: A

Corporate Accounting and Reporting

Standard (Revised Edition): Chapter 4

(Setting Operational Boundaries)

Scope 2

Indirect (upstream) generation

emissions of purchased or acquired

energy.

The Greenhouse Gas Protocol: A

Corporate Accounting and Reporting

Standard (Revised Edition): Chapter 4

(Setting Operational Boundaries)

Scope 3

All other indirect (upstream or

downstream) emissions that occur as a

consequence of the reporting

organization’s activities, but occur from

sources not owned or controlled by the

reporting organization.

The Greenhouse Gas Protocol: A

Corporate Accounting and Reporting

Standard (Revised Edition): Chapter 4

(Setting Operational Boundaries)

Organizational

boundary

Defines the boundary of direct and

indirect emissions for operations that fall

within a reporting organization’s

established organizational boundary.

The Greenhouse Gas Protocol: A

Corporate Accounting and Reporting

Standard (Revised Edition): Chapter 3

(Setting Organizational Boundaries)

Operational

boundary

The assignment of emissions sources

into scope 1, scope 2, or scope 3 once

the organizational boundary has been

set.

The Greenhouse Gas Protocol: A

Corporate Accounting and Reporting

Standard (Revised Edition): Chapter 4

(Setting Operational Boundaries)

Inventory accounting

(also called

attributional

accounting)

Accounts for GHG emissions or

removals within a defined organizational

and operational boundary.

https://ghgprotocol.org/blog/inventory-

and-project-accounting

Project-based

accounting (also

called intervention or

consequential

accounting)

Accounts for the impacts or changes in

GHG emissions resulting from specific

projects, actions, or interventions

relative to a counterfactual baseline

scenario. It evaluates system-wide

emissions impacts of the project or

intervention in question, without regard

to the reporting organization’s

operational or organizational inventory

boundary.

https://ghgprotocol.org/blog/inventory-

and-project-accounting

Scope 2 terms

Summary

Please read

Dual reporting

A requirement for scope 2 emissions to

be reported using two different methods:

a location-based method and a market-

based method.

GHG Protocol Scope 2 Guidance:

Chapter 6 (Calculating Emissions) and

Chapter 7 (Accounting and Reporting

Requirements)

Location-based

method

Scope 2 emissions that account for the

average emissions characteristics of the

grid from which energy is purchased.

GHG Protocol Scope 2 Guidance:

Chapter 4 (Scope 2 Accounting

Methods)

Market-based

method

Scope 2 emissions that account for a

organization’s contractual instruments

for specified energy (or its lack of choice

in purchasing specified energy).

GHG Protocol Scope 2 Guidance:

Chapter 4 (Scope 2 Accounting

Methods)

Scope 2 data

hierarchy

A hierarchy of instruments and data

sources for calculating market-based

scope 2 emissions at different levels of

accuracy.

GHG Protocol Scope 2 Guidance:

Chapter 6 (Calculating Emissions)

Scope 2 Quality

Criteria

A set of criteria for determining whether

a given contractual instrument can be

used to make a market-based scope 2

claim for a given quantity of energy

consumption.

GHG Protocol Scope 2 Guidance:

Chapter 7 (Accounting and Reporting

Requirements)

Page 6 of 27 @cdp | www.cdp.net

2 Introduction to scope 2

The GHG Protocol Corporate Standard divides an organization’s GHG emissions inventory into

direct and indirect emissions.

Direct emissions are emissions from sources that are owned and controlled by the reporting

organization.

These are scope 1 emissions.

Indirect emissions are emissions that are a consequence of the activities of the reporting

organization, but occur at sources owned or controlled by another organization.

Scope 2 emissions are the upstream indirect generation emissions of purchased or

acquired energy.

Scope 3 emissions are all other indirect (upstream or downstream) emissions that occur as

a consequence of the reporting organization’s activities, but occur from sources not owned

or controlled by the reporting organization.

Scope 2 emissions are given their own category of indirect emissions for several reasons. Firstly,

emissions from energy generation are one of the leading sources of global emissions (electricity

generation accounts for nearly a quarter of all GHG emissions). Secondly, almost every

organization purchases electricity, heat, steam, or cooling for its operations, and accurate data

exists to relate use of purchased energy to GHG emissions (quantity of energy consumption

multiplied by an emissions factor). The GHG Protocol Corporate Standard considers scope 3 an

optional disclosure category, but requires all reporting companies to report a minimum of both

scope 1 and scope 2 emissions.

2.1 Key concepts in scope 2 that impact your reporting to CDP

The Scope 2 Guidance formalizes two methods for calculating scope 2 emissions: the location-

based method and the market-based method.

Further reading to compare both methods: Table 4.1 in the Scope 2 Guidance.

2.1.1 Location-based method

Location-based scope 2 emissions account for the average emissions characteristics of the grids

where energy consumption occurs.

Further reading: 4.1.1 in the Scope 2 Guidance.

2.1.2 Market-based method

Market-based scope 2 emissions account for the emissions from energy that the reporting

organization has actively chosen (or its lack of choice). Many markets offer consumer choice in

energy procurement, or, more accurately, contractual instruments that convey property rights to

energy attributes. This means it is possible to consume energy from a grid that has a mix of

generation resources on it, but claim to use the energy from specific resources, and report those

resources’ generation emissions under the market-based method.

Section 3.2 elaborates on how your contractual instruments should be reported to CDP.

Further reading: 4.1.2 in the Scope 2 Guidance.

2.1.3 Dual reporting

Companies must report both location-based and market-based scope 2 emissions if they have

any operations in markets that offer the possibility of reporting market-based scope 2 emissions.

A reporting organization will report only a location-based scope 2 disclosure only if it exclusively

operates in markets that do not offer the possibility of reporting market-based scope 2 emissions.

In practice, virtually every organization reporting to CDP must dual report (see Section 4.1).

Page 7 of 27 @cdp | www.cdp.net

Further reading: Figure 6.1 in the Scope 2 Guidance.

2.1.4 The emissions rate approach

An emissions rate approach describes how almost all GHG emissions inventories are calculated

because it is usually not possible or practical to directly measure the GHG emissions being

accounted for. While many sources of scope 1 emissions can be directly measured (for example,

process or fugitive emissions) by the reporting organization, it is often necessary to use directly

available ‘activity data’ that quantify the activity that caused the GHG emissions. Activity data are

multiplied by an emissions factor to derive the GHG emissions the activity was associated with.

In scope 2, the activity data is the quantity of energy consumption that occurs, usually directly

measured through a meter (but possibly estimated) and stated on an energy supplier bill. The

source of emissions factors will vary depending on whether location-based emissions or market-

based emissions are being attributed to the quantity of energy consumption (see Section 4.2).

Further reading: 4.2 in the Scope 2 Guidance.

2.1.5 Scope 2 data hierarchies

Scope 2 emissions factors come from a variety of sources varying in their granularity (precision) in

both space and time.

Location-based emissions factors may attribute emissions from regional or subnational grids or the

national grid average.

The market-based emissions factors to choose are dictated by what contractual instruments the

reporting organization holds. These similarly attribute emissions with varying degrees of precision.

Further reading: Tables 6.2 and 6.3 in the Scope 2 Guidance.

2.1.6 Market-based Scope 2 Quality Criteria

The Scope 2 Guidance introduces Quality Criteria that a contractual instrument used to make a

market-based scope 2 claim must meet.

Section 4.3 elaborates how you should report on how your market-based scope 2 inventory

observes these Criteria.

Further reading: Table 7.1 in the Scope 2 Guidance.

2.1.7 Inventory and project-based accounting

Scope 1, scope 2, and scope 3 describe a reporting organization’s GHG inventory, and use an

inventory accounting concept (sometimes called attributional accounting). Inventory accounting

attributes GHG emissions or removals that have occurred to an organization. In contrast, project-

based accounting (sometimes called intervention or consequential accounting) measures the

consequence of a project on emissions relative to a counterfactual baseline scenario in which the

project does not exist. Project-based accounting methods are used, for example, to quantify the

issuance of carbon credits. Project-based methods cannot be used to describe a GHG inventory

because a GHG inventory does not compare itself with a counterfactual baseline scenario.

This means a carbon credit cannot be used in a scope 1, scope 2, or scope 3 emissions total.

Emissions reductions from carbon credits are reported separately from the inventory total.

This does not mean that actions taken to reduce scope 2 emissions (such as purchasing

renewable energy) are not associated with a consequential avoided emissions effect. It only means

such effects are not accounted for in scope 2. Review 6.9 in the Scope 2 Guidance for more

information on how such effects can be reported on in optional disclosures separately from the

scopes. CDP does not currently capture avoided emissions claims except those based on

purchases of carbon credits.

Further reading:

• Inventory and Project Accounting: A Comparative Review (blog post, GHG Protocol,

2023)

Page 8 of 27 @cdp | www.cdp.net

• 8.2.4 and 6.9, and Chapter 10 in the Scope 2 Guidance

3 Reporting your scope 2 emissions to CDP

3.1 Scope 2 emissions targets, totals, breakdowns, and intensity

metrics

Question-specific guidance:

7.53.1: Provide details of your absolute emissions targets and progress made against

those targets.

• Please note that this refers to 7.53.2 as well.

• As some companies will be calculating two Scope 2 figures (market-based and location-

based), they may wish to set specific targets for each figure. For example, a organization

may intend to reduce their market-based figure through the purchase of renewable energy

certificates, which would decrease that figure, but would not impact their location-based

figure. This is just one approach to reducing emissions, and an organization may also

decide to set a location-based target focused on decreasing energy consumption and

improving energy efficiency. Thus, an organization can set targets for a location-based

figure, a market-based figure, or potentially both.

7.54.1: Provide details of your targets to increase or maintain low-carbon energy

consumption or production.

• Targets related to increasing low-carbon energy consumption or production are an

important element of organizations’ strategy to reduce their Scope 2 emissions.

o This question does not require any Scope 2 data inputs, but can be linked to an

emission target from question 7.53.1 in Column 16 “Is this target part of an emissions

target?”

7.5: Provide your base year and base year emissions.

• Companies should ensure that the base year inventory includes both a location-based

and market-based Scope 2 total, if applicable.

7.3: Describe your organization's approach to reporting Scope 2 emissions.

• Question 7.7 allows an organization to report their Scope 2 emissions using both the

location-based and market-based approach, in accordance with the GHG Protocol’s

Scope 2 Guidance. Question 7.3 allows an organization to explain why they may not be

providing a market-based emissions figure.

7.7: What were your organization's gross global Scope 2 emissions in metric tons

CO

2

e?

• Companies are asked to provide both their Scope 2 figures (if applicable).

• You may use the comment column to add information around the data source(s) for your

location-based emissions, such as the granularity of the calculation. You can also note, if

you are reporting market-based emissions, whether a location-based emissions factor has

been used to calculate any market-based emissions due to unavailability of a residual mix

factor. You should note, if you are reporting market-based emissions, any noncompliance

with the Scope 2 Quality Criteria.

7.45: Describe your gross global combined Scope 1 and 2 emissions for the reporting

year in metric tons CO

2

e per unit currency total revenue and provide any additional

intensity metrics that are appropriate to your business operations.

• Companies are required to disclose their emissions intensity for combined Scope 1 and 2

emissions against their total revenue for the reporting year, as well as at least one other

metric of their choice. However, companies are required to be transparent about which

Scope 2 figure they use. Companies should specify this in column 5 “Scope 2 figure

used”.

7.16: Break down your total gross global Scope 1 and 2 emissions by country/area.

• Please note that this refers to 7.20.1, 7.20.2 and 7.20.3 as well.

Page 9 of 27 @cdp | www.cdp.net

• CDP asks companies to provide a breakdown of Scope 2 figures. For example,

companies are asked to breakdown their Scope 2 figures down by country/area/region,

business activity, facility and emissions by activity. Each of these questions have columns

for companies to provide a breakdown of their Scope 2 location-based market-based

emissions. The purpose of CDP requesting these breakdowns is to increase transparency

on how they were calculated. E.g. an organization may be required to provide both a

market-based and location-based Scope 2 figure, but may also have operations in a

country/area where there are no contractual instruments. By providing a country/area-

specific breakdown, an organization can increase transparency on where there are

contractual instruments.

7.10.2: Are your emissions performance calculations in 7.10 and 7.10.1 based on a

location-based Scope 2 emissions figure or a market-based Scope 2 emissions figure?

• In question 7.10.1, companies are asked to compare their combined Scope 1 and 2

emissions to the previous reporting year. Companies are only required to compare their

Scope 2 emissions for just one Scope 2 figure (either location-based or market-based). In

the interest of transparency, companies are required to state which figure they used.

• A organization may not have calculated a market-based figure in the previous reporting

year. In this case, an organization can recalculate the previous year figure according to

the market-based principles, and then compare it with the current reporting year’s market-

based figure.

3.2 Your activity data and your contractual instruments

In addition to providing scope 2 totals, breakdowns, targets, and intensity metrics, you can also

disclose the underlying activity data and contractual instruments that were used in the calculation

of your scope 2 emissions. These are captured in module 7 (Environmental Performance – Climate

Change) in the Corporate Questionnaire.

7.30.1: Report your organization’s energy consumption totals (excluding

feedstocks) in MWh.

• This question captures your total consumption of purchased electricity, heat, steam,

and cooling underlying your scope 2 emissions disclosure

7.30.18: Provide a breakdown by country/area of your electricity/heat/steam/cooling

consumption in the reporting year.

• This question captures a country/area breakdown of the disclosures in 7.30.1 to

help understand the scope 2 intensities by country/area reported in 7.16.

7.30.14: Provide details on the electricity, heat, steam, and/or cooling amounts that

were accounted for at a zero or near-zero emission factor in the market-based Scope

2 figure reported in 7.7.

• This question captures the contractual instruments that gave you claims to zero or

near-zero market-based scope 2 emissions for certain quantities of use of

purchased energy. See Section 4.3 to understand how the Scope 2 Quality Criteria

impact this question.

• RE100 companies are shown equivalent questions 7.30.17 and 7.30.18.

Page 10 of 27 @cdp | www.cdp.net

4 What scope 2 requirements impact your response?

‘Shall’ in the Scope 2 Guidance

The Scope 2 Guidance uses the word ‘shall’ for its minimum requirements. This chapter

summarizes each of the 'shall' statements in Chapter 7 of the Scope 2 Guidance (Accounting and

Reporting Requirements) and advises where in your CDP response your adherence to ‘shall’

statements can be evidenced.

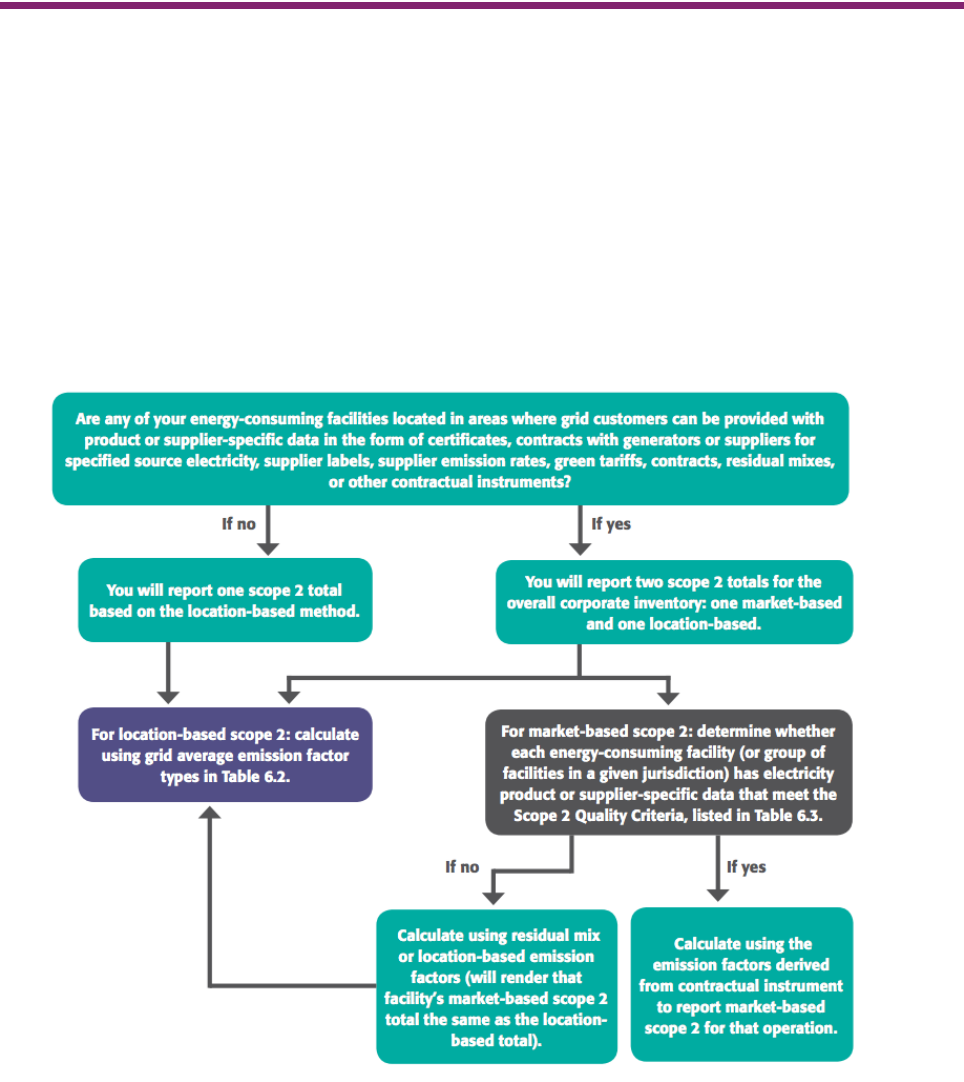

4.1 Determining whether you shall dual report

Figure 6.1 in the Scope 2 Guidance gives a decision tree for determining whether you shall dual

report scope 2 emissions, and guides you through finding the appropriate emissions factors to

cover your energy purchasing.

The overwhelming majority of companies reporting to CDP disclose operations in at least one

country or area where grid customers can be provided with product or supplier-specific data in the

form of certificates or contracts with generators or suppliers for specified sources of energy,

supplier labels, supplier emission rates, green tariffs, contracts, residual mixes, or other contractual

instruments. Based on the 2023 disclosure cycle, only six out of more than 23,000 companies

disclosed operating exclusively in countries or areas that would imply they only needed to disclose

location-based scope 2 emissions.

In the 2023 disclosure cycle, only 26% of companies reporting to CDP dual reported their scope 2

emissions.

How to report in line with the Scope 2 Guidance to CDP:

In question 7.7, dual report your scope 2 emissions if dual reporting applies to you.

Page 11 of 27 @cdp | www.cdp.net

4.2 Choosing the right emissions factors (scope 2 data hierarchy)

After understanding whether dual reporting applies, you must select emissions factors to pair with

consumption of purchased energy. Location-based emissions will be calculated using location-

based emissions factors for different geographic areas paired with the consumption of purchased

energy in those geographic areas. Market-based emissions will be calculated using market-based

emissions factors you are entitled to through contractual instruments, paired with the consumption

of purchased energy consumed through each contractual instrument.

4.2.1 Emissions factors for market-based accounting

4.2.1.1 EACs and contracts

Energy attribute certificates (EACs) are standardized, tradable instruments issued to a unit of

energy generation (usually, by MWh). These certify the origin of energy and convey property rights

to energy attributes. They may be purchased with energy as a bundled supply or purchased

unbundled from energy. EAC registries exist in many countries. See Section 6 for country-level

resources on what EAC registries exist.

Where EACs have not been issued to the purchased energy, a contract can provide the emissions

factor. The contract must perform the equivalent tracking and property rights allocation functions

that EACs perform. Such contracts can be, for example, power purchase agreements (PPAs) with

grid connected generators and contracts with energy suppliers.

4.2.1.2 Supplier-specific emissions factor

Electricity suppliers supply electricity sourced from generation facilities that they operate and/or

that they have purchased from the electricity market for delivery to users. Suppliers may offer

specified products for electricity, certified through EACs or otherwise assigning specified

generation to specified customers contractually.

Location-based

method

1. Regional or

subnational grid

average

2. National

production

Market-based

method

1. Energy

attribute

certificates

(EACs) and

contracts

2. Supplier-

specific

emissions factor

3. Residual mix

4. Regional or

subnational grid

average

5. National

production

Page 12 of 27 @cdp | www.cdp.net

The remainder of a supplier’s electricity sales portfolio may not assign specified generation to

specified customers, but still reflects sales of electricity from a range of generation resources to a

group of energy consumers, from which a supplier-specific emissions factor can be defined.

From 6.11.3 in the Scope 2 Guidance:

“The emission factor must include all the electricity delivered by the supplier, including electricity

it generates as well as electricity it purchases from others. Some supplier emission factors only

include generation facilities owned by the supplier, which does not represent the full electricity

delivered. In addition, it should only include renewables for which RECs have not been passed

on to and retired by a third party.”

The Scope 2 Guidance recommends that supplier-specific emissions factors be calculated using

the methodology provided by the Climate Registry Electric Power Sector (EPS) Protocol. This

methodology produces supplier-specific emissions factors that account for the attributes of

generation from facilities operated by the supplier and from facilities operated by others (i.e.

purchases from the electricity market), with or without certification through EACs. In practice,

CDP understands many supplier-specific emissions factors consider the owned generation

portfolio only (which leads to double counting if the supplier purchases electricity for re-sale), or

additionally only attribute emissions to purchased and re-sold electricity using the residual mix

(see below), which is less accurate than what the EPS Protocol methodology enables.

4.2.1.3 Residual mix

A residual mix emission factor represents the emissions and generation that remain after

certificates, contracts, and supplier-specific factors have been claimed and removed from the

calculation. It can be a regional or national factor. Residual mix factors are essential for accurate

scope 2 accounting because they capture the emissions of the generation resources (usually,

mostly fossil fuel resources) that have not been actively claimed by other companies through

EACs, equivalent contracts, or supplier-specific emissions factors.

4.2.1.4 Other grid average emissions factors

Following the hierarchy, when emissions factors from certificates, contracts, suppliers or the

residual mix are not available, you must use regional or subnational grid factors and, as an option

of last resort, national production factors in market-based accounting. If these factors are present

in your market-based scope 2 total, you shall disclose their use.

How to report in line with the Scope 2 Guidance to CDP:

In in column 4 “Methodological details” in question 7.7, declare if any market-based

emissions were calculated using location-based emissions factors to cover the absence of

a residual mix or other more precise market-based emissions factor.

Page 13 of 27 @cdp | www.cdp.net

4.3 Scope 2 Quality Criteria

Please see section 7.5 in the Scope 2 Guidance for more detailed guidance on each

criterion.

CDP is frequently asked for its view around time matching (vintage) requirements (Quality Criterion

#4), and location matching (market boundary) requirements (Quality Criterion #5).

4.3.1 Vintage limitations for purchased electricity

For a twelve-month reporting period, CDP recommends a vintage limitation of six months before

the start of the reporting period, the twelve months of the reporting period, or three months after

the end of the reporting period. This is a 21-month vintage limitation common to some international

voluntary green power programs. CDP has not developed a view on this Quality Criterion for heat,

steam, or cooling.

All contractual instruments used in the market-based method for scope 2 accounting

shall:

1. Convey the direct GHG emission rate attribute associated with the unit of electricity

produced.

2. Be the only instruments that carry the GHG emission rate attribute claim associated

with that quantity of electricity generation.

3. Be tracked and redeemed, retired, or canceled by or on behalf of the reporting entity.

4. Be issued and redeemed as close as possible to the period of energy consumption to

which the instrument is applied.

5. Be sourced from the same market in which the reporting entity’s electricity-consuming

operations are located and to which the instrument is applied.

In addition, utility-specific emission factors shall:

6. Be calculated based on delivered electricity, incorporating certificates sourced and

retired on behalf of its customers. Electricity from renewable facilities for which the

attributes have been sold off (via contracts or certificates) shall be characterized as

having the GHG attributes of the residual mix in the utility or supplier-specific emission

factor.

In addition, companies purchasing electricity directly from generators or consuming

on-site generation shall:

7. Ensure all contractual instruments conveying emissions claims be transferred to the

reporting entity only. No other instruments that convey this claim to another end user

shall be issued for the contracted electricity. The electricity from the facility shall not

carry the GHG emission rate claim for use by a utility, for example, for the purpose of

delivery and use claims.

Finally, to use any contractual instrument in the market-based method requires that:

8. An adjusted, residual mix characterizing the GHG intensity of unclaimed or publicly

shared electricity shall be made available for consumer scope 2 calculations, or its

absence shall be disclosed by the reporting entity.

Page 14 of 27 @cdp | www.cdp.net

4.3.2 Market boundaries for electricity-related scope 2 claims

The Scope 2 Guidance does not give a concrete list of markets, but refers to the following

characteristic elements of markets:

Areas of production and consumption of energy that are linked by transmission

infrastructure.

Areas where certificates may be traded and redeemed, retired or canceled, as defined by

regulatory authorities and/or certificate issuing bodies.

Political or regulatory boundaries that define recognition of energy-related contractual

instruments.

The boundaries of the residual mix calculation.

This guidance is frequently misinterpreted or ignored by companies reporting market-based scope

2 emissions for their consumption of purchased electricity that undertake ‘global matching’.

In the absence of any global implementation of ‘market boundaries’ for purchased electricity,

CDP maintains a definition. A market for electricity-related scope 2 claims is an area where:

The laws and regulatory framework governing the electricity sector are consistent

between the areas of production and consumption.

There is physical interconnection between generation and consumption.

Utilities/energy suppliers recognize each other’s energy sourcing instruments and have

a system in place to prevent double counting of claims.

These conditions describe, almost universally, national borders.

CDP recognizes the following international markets for electricity-related scope 2 claims:

1. The single market between the United States and Canada.

2. The single market in Europe, defined below.

Countries in Europe meeting all the following conditions form a market for electricity-related

scope 2 claims:

1. The country is in the EU single market; and

2. The country is a member of the Electricity Scheme Group and issues European

Energy Certificate System (EECS) Guarantees of Origin; and

3. The country has a grid connection to another country meeting the first two rules.

As of March 2024, the European countries meeting these criteria to form a single market for

electricity-related scope 2 claims are:

Austria

Germany

Norway

Belgium

Greece

Portugal

Croatia

Hungary

Slovakia

Czech Republic

Italy

Slovenia

Denmark

Latvia

Spain

Estonia

Lithuania

Sweden

Finland

Luxembourg

Switzerland

France

Netherlands

European microstates*

*The Channel Islands, Andorra, Liechtenstein, Monaco, San Marino, and Vatican City are included in CDP’s view of

a market for electricity-related scope 2 claims in Europe despite not meeting all three European market criteria.

This because they have limited domestic electricity generation and instead import much of their electricity, including

EECS GOs, from bordering Electricity Scheme Group member countries. Here, companies may make electricity-

related scope 2 claims based on ex-domain cancellation of EECS GOs.

Page 15 of 27 @cdp | www.cdp.net

How to report in line with the Scope 2 Guidance to CDP

In question 7.7, you may describe how much of your market-based emissions disclosure

does not meet the Scope 2 Quality Criteria. Use CDP’s market boundary definition for

electricity purchasing. As in Section 0, declare if a location-based factor was used in the

market-based total to cover the absence of a residual mix for any energy consumption.

4.4 If you consume energy from facilities that you own/operate

Energy you consume from facilities you own/operate is normally not associated with scope 2

because the your ownership puts the facility in your scope 1 boundary. However, if the attributes of

the energy you consume from your facilities are not retained by your organization (e.g. any

certificates are sold, or a contract entitles another organization to the attributes), then you shall

report market-based scope 2 emissions for this energy consumption (using the residual mix

emissions factor if available). See Table 6.1 in the Scope 2 Guidance for more information.

4.5 If you consume purchased energy generated from biofuels

Biogenic CO2 generation emissions associated with your energy purchasing are not accounted for

in scope 2. These emissions are reported separately from the scopes. See 6.12 in the Scope 2

Guidance. You may report on your biogenic CO2 emissions in question 7.12.1 in the CDP

Corporate Questionnaire.

Page 16 of 27 @cdp | www.cdp.net

5 Optional scope 2 disclosures

Please read Chapter 8 in the Scope 2 Guidance for more detail on GHG Protocol’s

recommended reporting on instrument features and policy context for scope 2.

How can companies go further with their Scope 2 reduction action? Section 11.4 of the GHG

Protocol Scope 2 Guidance presents a range of procurement choices where companies can bring

to bear their financial resources, creditworthiness, scale of consumption, technical knowledge,

collaboration, or other approaches in order to help overcome traditional barriers to scaling the

development of low-carbon energy.

These include a) Direct contracting with new low-carbon energy projects, b) working with electricity

suppliers for new projects, c) establishing “eligibility criteria” for corporate energy procurement,

relating to specific energy generation features or policy interactions that align with new low-carbon

energy projects, and d) incremental funding or donations.

Companies can also help drive more impactful procurement by choosing projects based on their

commissioning year. Progress towards zero carbon grids at scale requires new renewable

electricity generation and focusing procurement on new projects can help support new generation.

Matching procurement geographically and/or temporally is another way to go further. Matching an

organization’s consumption of electricity with their procurement at e.g. the regional and the hourly

level will create demand for the necessary low-carbon energy generation at specific times of day in

their specific regions. This may require additional labels or attributes, such as hourly EACs issued

under EnergyTag’s Granular Certificate (GC) Scheme Standard.

Additional, voluntary labels are a way for companies to do more with their purchases. Green-e

certification is one example. It is a leading certification program for renewable energy in North

America. The additional label certifies that the renewable energy must be generated from new

facilities, marketed with complete transparency and accuracy, and delivered to the purchaser, who

has sole title.

The GHG Protocol Scope 2 Guidance mentions the EKOenergy label

1

as an option, as it is a mark

of quality which comes on top of tracking certificates. Electricity sold with the EKOenergy label

fulfils strict environmental criteria and raises funds for new renewable energy projects.

Involvement, transparency and ‘deeds not words’ are important principles of EKOenergy’s work.

Another example is Gold Standard, an international standard for climate security and sustainable

development. Gold Standard

2

has developed an ecolabel for attribute tracking systems including

for use in combination with the I-REC Standard, EECS-GOs in Europe and other national/regional

systems adherent to their quality standards. The Gold Standard REC label includes stringent

requirements to ensure renewable energy projects meet highest safeguards, are inclusive of

stakeholders, contribute to sustainable development priorities, and generate new renewable

energy that could not have otherwise been realized.

5.1.1 How to report in line with the Scope 2 Guidance to CDP

Much of this optional reporting can be disclosed in 7.30.14 (7.30.17 and 7.30.18 for RE100

companies). Chapter 8 of the Scope 2 Guidance also calls for country/area or other

breakdowns of scope 2 emissions and underlying energy consumption, which are captured

by CDP throughout the corporate questionnaire.

1

https://www.ekoenergy.org/ecolabel/

2

https://www.goldstandard.org/our-story/sector-renewable-energy

Page 17 of 27 @cdp | www.cdp.net

6 Country/area resources for emissions factors

6.1 Location-based emissions factors

Many countries’ governments will publish a scope 2 location-based emissions factor for their

grid(s).

The International Energy Agency (IEA) maintains a list of scope 2 location-based emissions

factors.

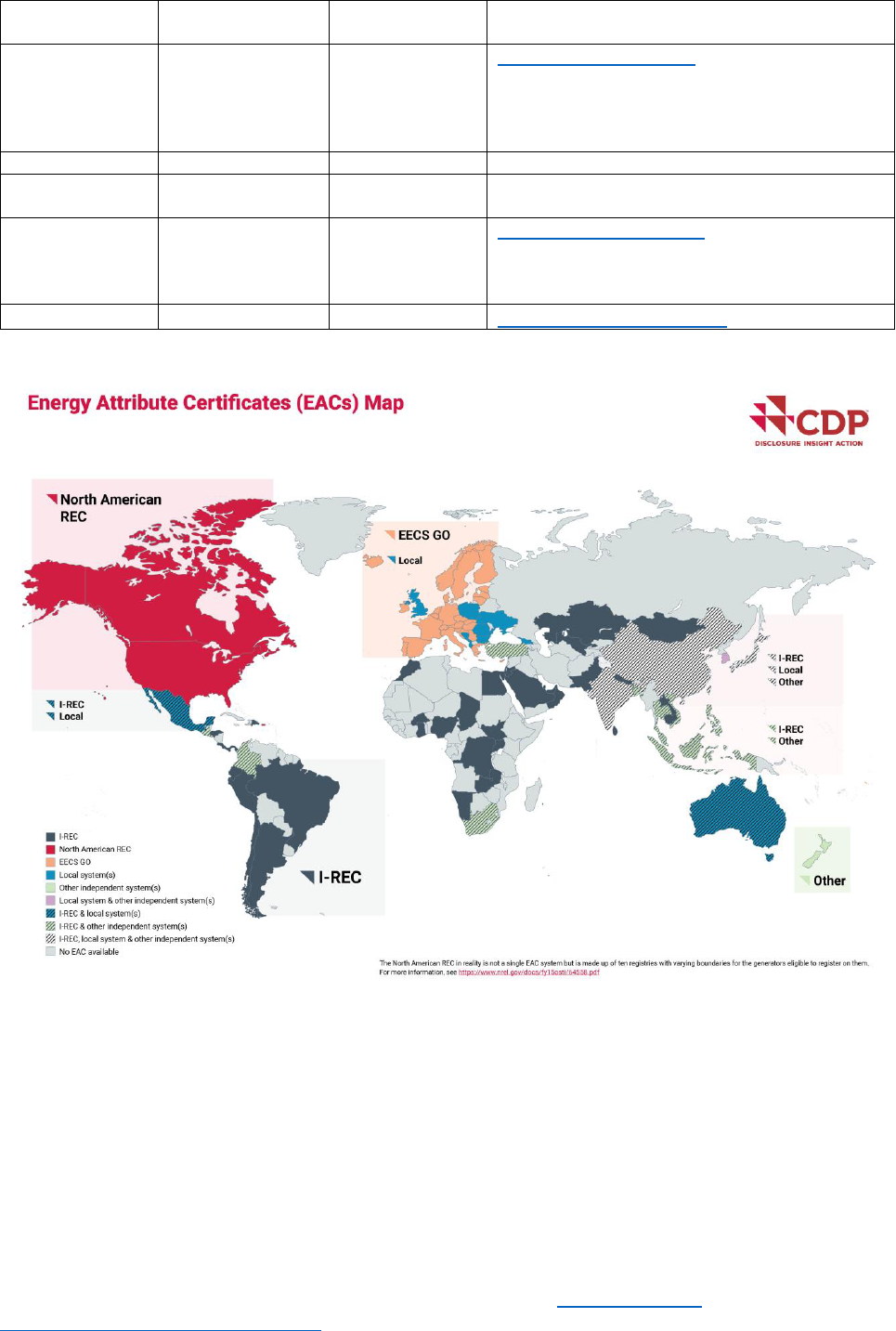

6.2 Energy attribute certificate registries

EACs from the following systems appear in companies’ reporting to CDP:

EAC system

Governance

Country/areas

served

Additional resources/comment

Renewable

Energy

Certificate

(REC)

Government-run

U.S. and

Canada

The North American REC in reality is not a

single EAC system but is made up of ten

registries with varying boundaries for the

generators eligible to register on them. For

more information, see

https://www.nrel.gov/docs/fy15osti/64558.pdf

Guarantee of

Origin (GO)

Government-run

Europe

The Association of Issuing Bodies (AIB)

maintains a system called the European

Energy Certificate System (EECS), which

standardizes GO issuance and trade across

AIB member states in the Electricity Scheme

Group. These states issue EECS GOs. GOs

issued by non-member states are sometimes

referred to as ‘national GOs’, and are not part

of a harmonized system.

Renewable

Energy

Guarantee of

Origin (REGO)

Government-run

United Kingdom

T-REC

Independent

Taiwan, China

Non-Fossil

Certificate

(NFC)

Government-run

Japan

Green Electricity

Certificate

Independent

Japan

J-Credit

Government-run

Japan

Tradable

Instruments for

Global

Renewables

(TIGR)

Independent

Green Electricity

Certificate

(GEC)

Government-run

China

I-REC for

Electricity

Independent

At least 48

countries

https://www.trackingstandard.org/product-

code/electricity/

Large-scale

Generation

Certificates

(LGCs)

Government-run

Australia

https://www.cleanenergyregulator.gov.au/RET/

Scheme-participants-and-industry/Power-

stations/Large-scale-generation-certificates

Small-scale

Technology

Certificates

(STCs)

Government-run

Australia

https://www.cleanenergyregulator.gov.au/RET/

Scheme-participants-and-industry/Agents-and-

installers/Small-scale-technology-certificates

Page 18 of 27 @cdp | www.cdp.net

EAC system

Governance

Country/areas

served

Additional resources/comment

New Zealand

Energy

Certificate

System

(NZECS)

Independent

New Zealand

https://bravetrace.co.nz/

Indian REC

Government-run

India

Korean REC

Government-run

Republic of

Korea

Yenilenebilir

Enerji Kaynak

Garanti Sistemi

(YEK-G)

Independent

Turkey

https://yekgnedir.com/en/

zaREC

Independent

South Africa

https://www.recsa.org.za/

6.3 Supplier-specific emissions factors

CDP is not resourced or organized to detail all countries where supplier-specific emissions factors

are available. Generally, fuel mix disclosure (FMD) legislation like what exists in the European

Union is a form of evidence that supplier-specific emissions factors are available. However, FMD

legislation may typically only require a supplier to publicly disclose the generation mix and

emissions profile of the generation that it owns, not the total supply of energy to consumers

sourced from both its own generation facilities and energy markets.

6.4 Residual mixes

Residual mixes for European countries are published by AIB: https://www.aib-

net.org/facts/european-residual-mix

Page 19 of 27 @cdp | www.cdp.net

Green-e publishes residual mixes for U.S. eGrid subregions that remove Green-e® Energy sales.

These are incomplete residual mixes, since they only account for and remove specified energy

certified by Green-e, which does not represent all specified energy sales.

The International Tracking Standard Foundation (I-TRACK) is working on calculating residual

mixes for countries with I-REC registries. It is unclear whether these residual mixes will account

only for and remove energy certified by I-RECs or whether they will also account for and remove

energy tracked through other EAC systems or contracts.

Residual mixes are not widely available.

Page 20 of 27 @cdp | www.cdp.net

7 Frequently Asked Questions

7.1.1.1 Can I count a GO/REC/I-REC/TIGR towards my Scope 2 market-based target?

Yes.

7.1.1.2 Can I count certified emissions reductions (CERs) or verified emissions reductions (VERs)

towards my Scope 2 market-based target?

No.

7.1.1.3 I buy special European credits from a label with guaranteed additionality, but they do not

follow the GO system, can I count them towards my target?

CDP does not recommend that any electricity within the EU27 should be accounted for unless it is

using European Guarantees of Origin.

7.1.1.4 Can I use European GOs to account for electricity consumption in USA?

No, as this wouldn’t comply with the market boundary criteria as described in section 4.3.2. Please

see the next question for more details.

7.1.1.5 Why can’t I use RECs or certificates produced in certain jurisdictions in other

jurisdictions?

As a minimum condition, you should use RECs that are within the same market boundary as

described in section 4.3.2, e.g. if you have operations in North America, you are expected to use

RECs (USA and Canada) and not Guarantees of Origin (GOs), which are the instruments used in

Europe. Likewise, your European operations are expected to use GOs and not North American

RECs or other instruments from other geographies. Unlike offsets, electricity tracking

instruments are not expected to become global commodities, but regional commodities.

This is because there are physical restraints to the transmission of electricity that should be

respected by the tracking instrument trade. A good example is the case of islands, for example

Iceland. There is no connection between Iceland and mainland Europe. As such, buying Icelandic

GOs as a supply of European based consumption is seen as a problematic practice. These

considerations could be extended to reflect transmission capacity between countries, which could

add layers of complexity that, at the current stage of development of the system, are still difficult to

address. The best way to address them is to source renewable energy from local renewable

sources.

7.1.1.6 Can I use UK green tariffs in order to account for lower Scope 2 emissions?

Yes, depending on the tariff chosen. Some tariffs are 100% renewables, some are not, but the

supplier has the obligation to inform the customer about it.

Can I use an emission factor provided by my supplier?

Yes, in your market-based Scope 2 figure.

7.1.1.7 Where can I find corrected emission factors for the grid?

You should check with the relevant grid authority or regulator for up-to-date corrected emission

factors where available. For example, the AIB has calculated corrected grid emission factors for all

EU countries.

Page 21 of 27 @cdp | www.cdp.net

7.1.1.8 I purchase offsets that are based on renewable energy generation, can I account for these

in my Scope 2 figure?

No. In this case the origin of the offsets doesn’t really matter. According to the GHG Protocol

Corporate Standard, offsets should be reported as separate information from the gross emission

figures that Scope 1, 2 and 3 represent.

You can report your use of offsets in questions 7.79 and 7.79.1 where you can provide details of

any project-based carbon credits cancelled within the reporting period as well the purpose of those

purchases.

7.1.1.9 Can RECs/GOs/IRECs/TIGRs be reported in 7.79?

Question 7.79 only applies to companies that have issued the carbon credits or who have

purchased them for the purposes of compliance or as voluntary carbon offsets. Therefore, they

cannot be reported here.

7.1.1.10 If we purchased more RECs than the amount of energy we actually consumed (1 REC=

1MWh), can we then enter a negative Scope 2 figure?

No. RECs are not offsets – they are a way to attribute an organization’s energy purchase to a

renewable source and claim the low carbon benefit. That is why RECs are a regional product - the

energy used should be in the same market boundary as the energy produced and represented by

the certificate. Even if they were offsets, in accordance with the GHG Protocol, CDP asks

companies to report on gross emissions that do not take offsets under consideration. None of the

emission fields in the CDP questionniarewill allow a negative response for this reason.

7.1.1.11 We operate in a country that has 100% electricity from hydroelectricity. How should we

report this?

If the fuel mix in your national grid has a large proportion of renewable energy, then naturally your

carbon emissions per MWh are going to be lower than in countries that have a higher proportion of

fossil fuel-based sources in the grid mix, and therefore your Scope 2 emissions calculated with the

location-based method will be low. However, you should not report renewable energy usage which

is sourced from grid mix as active renewable energy procurement.

In countries where contractual instruments do exist, companies should report Scope 2 (market-

based) emissions using the emission factor provided by the contractual instruments, or the residual

mix emission factor. If your organization is not directly purchasing energy from renewable energy

providers, you should be using the residual mix emission factor. Only in countries where

contractual instruments or residual mix emission factors do not exist, can companies use the grid

average emission factor.

Page 22 of 27 @cdp | www.cdp.net

8 Worked examples

8.1 Example 1 – On-site production of non-grid connected

renewable electricity owned by another organization with no

tracking instruments generated.

It is becoming common for an organization to supply the space, while another organization

implements and manages the renewable energy installation that produces electricity. This

electricity can then be fed to the organization that is providing the space and consumed “on the

spot”. For the sake of this example we will assume the following energy profile of Organization 1:

It has multiple facilities (remote equipment, e.g. diesel generators) around the world that

consume small amounts of electricity, as well as large buildings that are grid connected;

It has installed solar panels at its facilities in Argentina which are owned and managed by

another organization; the 15,000 MWh generated by these solar panels are supplied to

Organization 1 and are subject to an agreement between the two parts which is equivalent to a

sale;

Their energy supplier in the USA provides them with a supplier-specific emissions rate;

For all other electricity, the organization is being supplied by the grid and does not have any

special agreements with its suppliers or buy and retire any type of certificates.

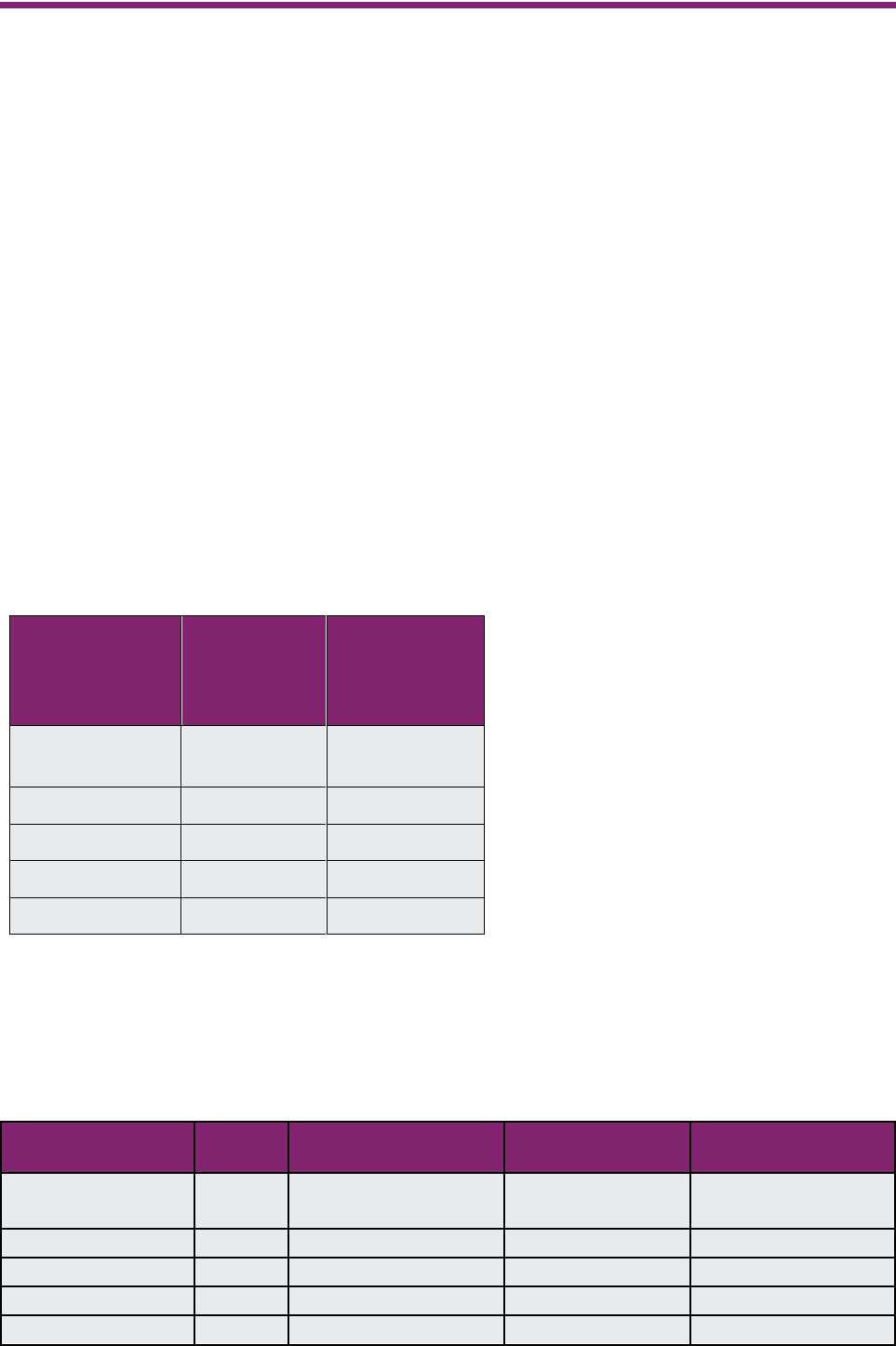

(7.16) Break down your total gross global Scope 1 and 2 emissions by country/region.

Country/Region

Scope 2,

location-

based (metric

tons CO

2

e)

Scope 2,

market-based

(metric tons

CO

2

e)

United States of

America

19,000

22,000

Canada

10,000

11,000

United Kingdom

30,000

32,000

Spain

10,000

13,000

Argentina

10,000

10,000

(7.30.1) Report your organization’s energy consumption totals (excluding feedstocks) in

MWh.

Since the organization is reporting a market-based Scope 2 figure, they should also use this in

7.30.1. They will thus use market-based methods to calculate the MWh from renewable sources for

this question. The table below details their calculations.

Country/region

Total

MWh

Emissions Factor

used

MWh from

renewable sources

MWh from non-

renewable sources

United States of

America

100,000

Supplier-specific

emissions rate (6.5%)

6,500

93,500

Canada

100,000

None

0

100,000

United Kingdom

140,000

Residual Mix (8,93%)

12,502

127,498

Spain

100,000

Residual Mix (7.51%)

7,510

92,490

Argentina

100,000

Contract

15,000

85,000

Page 23 of 27 @cdp | www.cdp.net

In Canada, they do not have energy certificates or contracts, supplier/utility-specific emission rates,

or a detailed residual mix. Therefore, to avoid double-counting by using grid average emissions

factors, they have assumed 0 MWh from renewable source. Similarly, in Argentina they have no

active sourcing outside of their contract and have assumed 0 additional MWh from renewables as

they do not have access to anything other than grid average emissions factors.

Based on these calculations, they would report the below in 7.30.1:

Activity

Heating

value

MWh from

renewable

sources

MWh from

non-renewable

sources

Total MWh

Consumption of fuel (excluding feedstock)

HHV

0

1,500,000

1,500,000

Consumption of purchased or acquired electricity

41,412

498,588

540,000

Consumption of purchased or acquired steam

0

100,000

100,000

Consumption of self-generated non-fuel

renewable energy

0

0

0

Total energy consumption

41,412

2,098,588

2,140,000

Page 24 of 27 @cdp | www.cdp.net

(7.30.14) Provide details on the electricity, heat, steam, and/or cooling amounts that were accounted for at a zero or near-zero emission factor in

the market-based Scope 2 figure reported in 7.7.

Country/area

of low-

carbon

energy

consumption

Sourcing

method

Energy

carrier

Low-carbon

technology

type

Low- carbon

energy consumed

via selected

sourcing method

in the reporting

year (MWh)

Tracking

instrument

used

Country/area of

origin (generation) of

the low-carbon

energy or energy

attribute

Are you able to

report the

commissioning or re-

powering year of the

energy generation

facility?

Commissioning

year of the energy

generation facility

Comment

Argentina

Purchase

from an on-

site

installation

owned by a

third party

(on-site

PPA)

Electricity

Solar

15,000

Contract

Argentina

Yes

2017

We have

established a

contract with Solar

Organization, a

provider of solar

energy solutions,

where they own

and manage all our

on-site installations

and we buy the

electricity from

them.

Page 25 of 27 @cdp | www.cdp.net

8.2 Example 2 – A organization purchasing RECs in the USA

Organization 1 is a USA based organization with installations in Oklahoma, California, Upstate

New York and Colorado. It consumes the following amounts of electricity:

Its Oklahoma facility also purchases 100,000 RECs (1 REC=1MWh) from an Oklahoma wind farm.

The facility is within the MROW eGRID sub-region, so when doing its calculations to compute the

electricity Scope 2 market-based footprint for MROW it uses the Green-e residual mix for the

portion of power it does not have RECs, this is 200,000 – 100,000 = 100,000 MWh. The 100,000

MWh for which it has RECs are computed using the specific RECs emission factor, which in this

case because it is a renewable energy source, will be assumed to be 0 t CO

2

e/MWh. Thus, the

footprint, calculated for each eGRID sub-region will look like the following table:

Total MWh

lb/MWh (Green-e Residual

Mix 2019)

t CO

2

e

MROW

(200,000 – 100 000) = 100,000

1,149.60

52,145

CAMX

150,000

461.46

31,397

RMPA

40,000

1,274.88

23,131

NYUP

30,000

232.36

3,162

Total USA

320,000

-

109,835

Thus, compared to the scenario where RECs would not have been bought, Organization 1 has

reduced its electricity market-based Scope 2 footprint by 64,644 t CO

2

e. The organization has also

consumed 10,000MWh of fuel (for energy purposes) during the reporting year.

Based on the published Green-e Residual Mix, the organization has calculated the % of MWh from

renewable sources in the eGRID sub-regions (CAMX = 44%, MROW = 30%, NYUP = 42%, RMPA

= 30%). Using these percentages, it calculates its MWh from renewable sources. Its CDP

disclosure would look like this:

(7.30.1) Report your organization’s energy consumption totals (excluding feedstocks) in

MWh.

Activity

Heating value

MWh from

renewable

sources

MWh from non-

renewable

sources

Total MWh

Consumption of fuel (excluding

feedstock)

HHV

0

10,000

10,000

MWh

MROW

200,000

CAMX

150,000

RMPA

40,000

NYUP

30,000

Total USA

420,000

Page 27 of 27 @cdp | www.cdp.net

(7.30.14) Provide details on the electricity, heat, steam, and/or cooling amounts that were accounted for at a zero or near-zero emission factor in

the market-based Scope 2 figure reported in 7.7.

Sourcing

method

Energy

carrier

Low-carbon

technology

type

Country/area

of low-carbon

energy

consumption

Tracking

instrument

used

Low- carbon

energy

consumed via

selected

sourcing

method in the

reporting year

(MWh)

Country/area of

origin

(generation) of

the low-carbon

energy or energy

attribute

Commissioning

year of the energy

generation facility

Comment

Unbundled

energy

attribute

certificates

(EACs)

purchase

Electricity

Wind

USA

US-REC

100,000

USA

2020

Organization 1 has

bought 100,000 RECs

from an Oklahoma wind

farm and reflected that in

its total Scope 2 footprint

provided in 7.7. This led

to a reduction of 64,644 t

CO

2

e from its market-

based footprint.